Fraina, who would return to this topic with several massive tomes in the 1930s, reviews the emergence of monopoly capitalism in the United States and some of the consequences–with a ‘middle class’ invested in large capital, what possible progressive role could they play?

‘Concentration, Monopoly, Competition: A New Economic Trend’ by Louis C. Fraina from New Review. Vol. 1 No. 13. September, 1913.

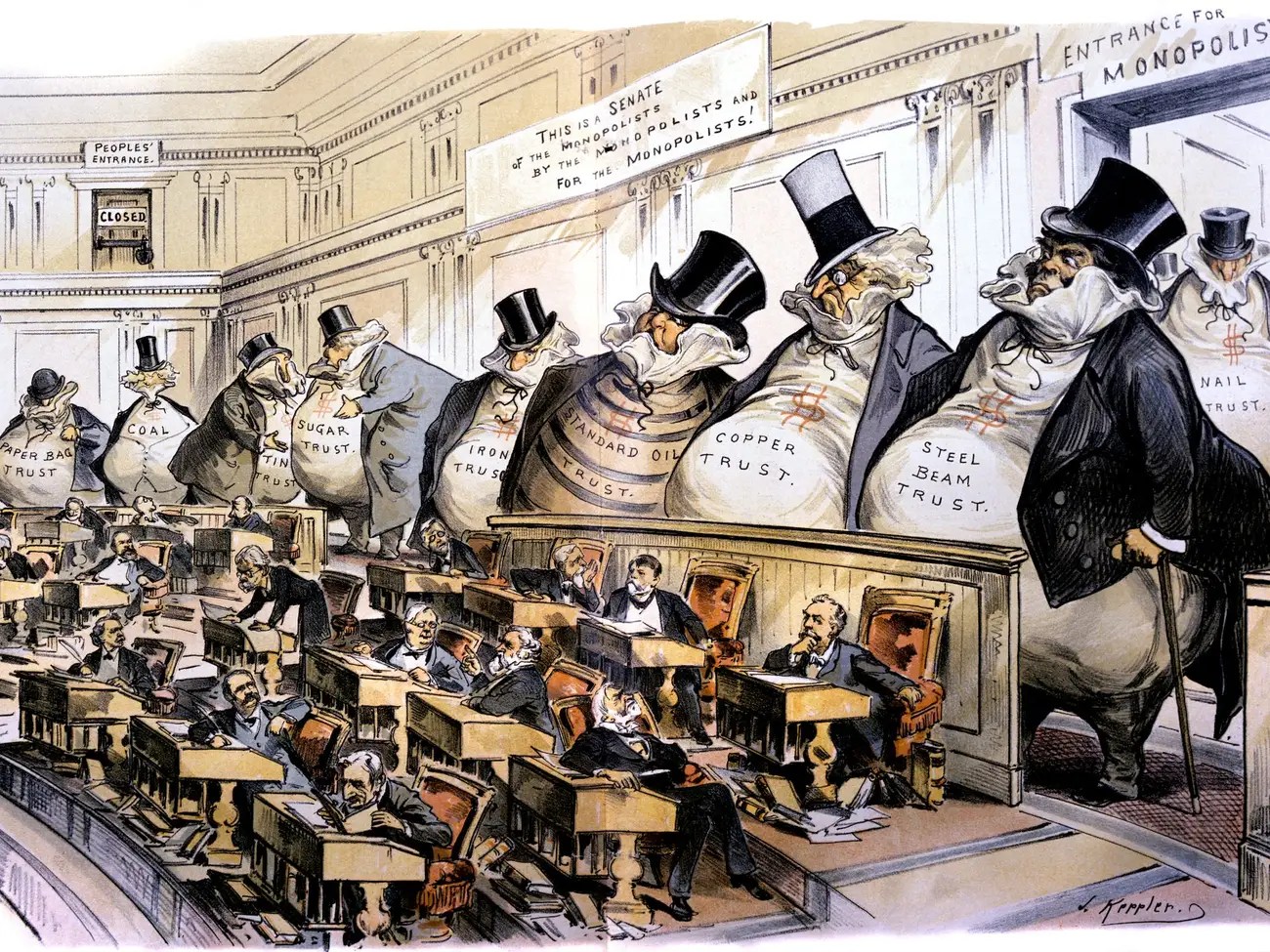

Critics hitherto indicted monopoly in the name of competition. Small capitalists in their despair assailed all forms of concentration. Chimerical schemes to curb monopoly were evolved. Monopoly, however, readily evades government dissolution decrees, the Standard Oil and Tobacco Trust “dissolutions” being monumental proof thereof. Attorney General McReynolds now holds that no trust can be adequately dissolved by a pro-rata distribution of the stock of its disintegrated parts among original stockholders, a community of interest being bound to exist. The new plan is to force ownership of disintegrated trusts into new hands–a problem of such magnitude as to defy governmental accomplishment. Nor is the accomplishment economically or mathematically possible. The scheme would be feasible if only a few trusts were concerned, and not the trust system as a whole. Considering the magnitude of trust-capital and the scattered, small-bulk nature of non-trust capital, the process of forcing ownership of all disintegrated trusts into new hands would ultimately resolve itself into the identical centralized ownership which now exists. While the merger of Union Pacific and Southern Pacific has been severed, a new merger has actually resulted–the practical merger of Union Pacific and Baltimore & Ohio. Prior to the dissolution, Union Pacific held $32,334,200 B. & O. common, and $7,206,400 preferred. Under the dissolution plan, U.P. bought about $40,000,000 of the Pennsylvania’s holdings in B. & O. The net result is that U.P. now controls the B. & O. policy. Indeed, the rumor prevails that with this new control and its considerable holdings in Vanderbilt roads, Union Pacific contemplates a trans-continental system. Simultaneously with this bankruptcy of government action, monopoly, or monopolistic centralization, is being indicted from a new source, from within monopoly itself; talk of restoring competition has virtually ceased, the new indictment being based on the “scientific” ground of efficiency.

The new economic trend aims not at disintegration or destruction, but at the readjustment of centralized capital, of the trust system.

This form of trust indictment developed immaturely a few years ago in the insurgent movement, typified by La Follette–an indictment made by powerful capitalists against the still more powerful capitalists of monopoly. The Insurgents aimed to restore a competition measured in terms of million-capitals. Judge Gary’s testimony a few months ago at the preliminary hearing in the Steel Trust dissolution suit illumines this competition. Discussing with J.P. Morgan the contemplated organization of the U.S. Steel Corporation, Gary stated that fair and reasonable competition, (competition between powerful aggregations of million-capitals such as prevails in the steel industry to-day) was a healthy stimulus, but that ruthless destructive competition was not only foolish but ultimately reacted upon the competitors.

The Insurgent movement, inevitably, coalesced around Roosevelt. La Follette hostilized concentration as much as plutocracy; his program was disintegrative and not readjustive. Roosevelt wishes to penalize monopoly’s abuses and monopoly itself, but to encourage concentration; his ideal is the steel industry, wherein Trust and “independents” harmoniously cooperate, enjoying the good in concentration and free from the evil in monopoly. This new economic trend is not of political origin, however. Its stimulus is economic, hence it controls politics.

President Mellen’s retirement from control of the New Haven transportation system was the first tangible result of this new trend. Mellen was a Morgan-Hill man, loyally supported in all his acts by that combine. Mellen was a disciple of Morgan and his faith in centralization. Morgan sustained Mellen against all attack. But since Morgan’s death and the realization in financial circles that his financial satrapy must be cast aside, interests identified with the Morgan group attacked Mellen, and met only with Mellen’s individual defense. The attack in financial circles was general. And Mellen was thrust aside. Not Brandeis and public indignation caused Mellen’s downfall, but the indifference and opposition of his former friends in Big Business. The New Haven system is now in process of readjustment, retaining the good in concentration, rejecting the evil in monopoly.

This economic trend is being accelerated from many sources. Secretary of Commerce Wm. C. Redfield, himself a large capitalist, addressing the American Cotton Manufacturers’ convention at Washington, April 9, 1913, said:

“It is alleged that the trusts are necessary for our industrial efficiency. There has been discussion altogether too brief, on the other hand, as to whether the trusts are as a matter of fact industrially efficient or not. A good many years ago the late Edward M. Shepard said to me that he believed the trust form of organization carried within itself the seeds of its own decay; that its economies were more apparent than real, and that the serious difficulty of obtaining the men who could manage efficiently with firm grasp and thorough control, these great organizations, would itself result in ultimate segregation. We are dealing with the trust in a sense as a national menace, whereas the fact may be that it menaces chiefly itself and the people interested in its securities.”

The argument is sound, made against monopoly; unsound, made against concentration. Monopoly does largely depend upon One-Man control. With the passing of financial giants such as Harriman and Morgan, the walls of the Jericho of monopoly threaten to fall.

One-Man control, necessary in monopoly, is a menace in another way. Trust officials use their power for personal profit. This is why economies are often “more apparent than real”. Under the head, “Do Trust Officials Secure Indirect Profits?” the New York Journal of Commerce of May 22nd last, quoted an authority as saying that a “large mill found that it has been robbed of more than $200,000 in the purchase of dye-stuffs”. There was extravagance in the purchase of practically all other material. “If a dominating executive of a company has a personal interest in concerns that sell supplies to his company, stockholders have not the slightest chance of receiving proper dividends.” Concerning a large industrial company whose stock was selling below par, this authority said:

“What is needed to secure a change is the selection of a board of directors, who will look after the affairs of the stockholders and will not be content to merely approve arbitrary acts of the president, who has entire control even to the smallest details.”

This strikes at the very root of monopoly, at the system of interlocking directorates through which the Morgan interests built up their intricate and gigantic monopoly. Interlocking directorates are inefficient, unwieldy. They are effective, and even then only temporarily and in a limited sense, when vitalized and integrated by the personality of a Morgan. Interlocking directorates promote industrial inefficiency, are an industrial menace. Their only justification lies in financial control, in monopoly.

Since monopoly does not promote industrial efficiency, its only value lies in ultimate control of prices. Until that control actualizes, industrial efficiency and profits are sacrificed. That was the Mellen-New Haven policy. In his efforts to monopolize New England’s transportation, Mellen sacrificed and lowered dividends, acquired control of competing water lines, bought up trolley systems, grasped connecting railroad lines far beyond his field of operation, and paid exorbitant prices for virtually useless properties; a process that, as one financial paper phrased it, “can only be justified in the event of monopoly being established to an extent that will permit monopolistic rates to be charged”. Recent events have shattered this dream of monopoly. We are at the threshold of a period when the federal government will regulate rates and prices. This regulation is welcomed by much of Big Business. Says Financial America (July 10, 1913): “Were it possible to substitute to-day the authority of the federal government over interstate carriers exclusively, it is an almost certain conclusion that few, if any, railroad officials would offer protest”.

In the Minnesota rate decision, the United States Supreme Court held that “the authority of the state to prescribe what shall be reasonable charges of common carriers for intrastate transportation unless it be limited by the exertion of the constitutional power of congress, is state-wide”. The federal government is supreme:

“If this authority of the state be restricted, it must be by virtue of the paramount power of congress over interstate commerce and its instruments; and in view of the nature of the subject a limitation may not be implied because of a dormant federal power, that is, one which has not been exerted, but can only be found in the actual exercise of federal control in such measures as to exclude this action by the state which, otherwise, would clearly be within its province.”

Many of the men in Big Business are in favor of government regulation of prices. Mr. Gary of the Steel Trust has repeatedly favored such regulation.

The era of monopoly, of monopolistic centralization, was typified by J. Pierpont Morgan. Upon his death, expressions were general that with him died the Morgan policy. The Journal of Commerce of April 7, said:

“A firm believer in centralization, he (Morgan) was probably the last of the old school of financiers who refused to bow to public opinion or to recognize the power behind public opinion to curb monopoly and centralization…There is no jealousy in the feeling that exists in some large banking circles that a successor to J. Pierpont Morgan is not needed.”

Moody’s Magazine expressed itself thus: “The era of Morgan that period from the final close of the Civil War, down to within the past year or two–is completed history”.

The identification of Morgan with the monopoly now being indicted is illuminating. Morgan was a financier; he neither directly created nor built up any great industry, such as Rockefeller did in Standard Oil. An analysis of the Morgan era in the light of monopoly, an analysis of monopoly in the light of the Morgan era, jointly illumine the new economic trend.

Centralization is financial, the financial unity of many capitals. Centralization may precede concentration, develop concentration, and be itself in turn developed by concentration Centralization plays an important part in capitalist development. “The world would still be without railroads if it had been obliged to wait until accumulation should have enabled a few individual capitals to undertake the construction of a railroad. Centralization, on the other hand, accomplished this by a turn of the hand through stock companies.” (Marx, “Capital”, Vol. I, Chap. XXV, Sec. 2.) Centralization accelerates economic expansion, breaks new ground and paves the way for systematic exploitation and development.

Centralization in America built great railroad systems and opened the West to exploitation. Centralization forged the tools which tapped great natural resources, and drew the whole of our continent into the circle of capitalist exploitation. Centralization gave impetus to new industries and supplied the means with which to build up new industries. If this process was accompanied by concentration and economic efficiency, that was partial and incidental–technically inevitable, but subjectively incidental. The primary object was grab, speculation, get-rich-quick. Monopoly was the necessary outcome of this process. The history of Morgan, Vanderbilt, Jay Gould, Harriman, Rockefeller, et al., is a history of grab, speculation, monopoly. New fields of endeavor invite these methods.

The magnates of the Morgan era accomplished mighty results in despite of their methods, the vast natural wealth of America practically compelling such results. Relatively, foreign capitalists, the Germans, for example, accomplished much more. There was small effort to systematize business, or create foreign trade; indeed, America’s foreign trade, considering her advantages, is a bagatelle.

In the capitalist scheme of things, this process performed mighty, effective work. Speculative centralization accomplished with almost lightning rapidity what plodding, systematic effort would have by now barely started. But this period is over, the pioneer work done. The extensive or expansive exploitation of the Morgan era is being succeeded by readjustment and intensive exploitation. In a world of superabundant natural wealth, Morgan et al. could acquire huge fortunes without considering efficiency or ultimate results. Now, with conservation in the air and the get-rich-quick conditions dead, efficiency and system are to have their inning.

The decline of Wall Street speculation is a symptom of this trend toward systematizing and readjusting the methods and tangled results of the Morgan era. Conditions described in Lawson’s “Friday the Thirteenth” are things of the past. Repeatedly of late have financial papers expressed the idea that Wall Street should become, in fact is fast becoming, purely an investment centre. Speculation on a huge scale died with the Morgan era.

Another symptom is the “industrial efficiency” movement. With system and readjustment, intensive methods are to be adopted, and the human unit in production is seen to possess hitherto undreamt of sources of surplus value. And, be it noted, the Steel Trust was a pioneer in this movement.

This readjustive trend in no way contemplates destruction of concentration, rather aims to promote concentration. Senator La Follette’s bill to amend the Sherman anti-trust law, introduced in the special session of congress, and defining a trust or “unreasonable restraint” of trade as control of 30 per cent. of the business in the United States in any commodity, was bitterly attacked by interests and papers active in the readjustive move. And Senator Hitchcock’s graduated tax amendment to the tariff bill, introduced at the instigation of Attorney General McReynolds and which in practice would tax Big Business out of existence, met with such a storm of opposition that the Senate Democratic caucus was compelled to reject the amendment. While there is to be a readjustment at the top, industrial concentration must not be interfered with. Tariff reduction and the Democratic threat to investigate and expose concerns trying to recoup their losses by lowering wages will undoubtedly stimulate concentration as the only way to meet new competitive conditions.

How will competition function under the new conditions? Competition will prevail within ever narrower limits. Competition is not dead, nor can original competition be restored. The new competition is between million-capitals. The dissolution of the Tobacco Trust stimulated competition, but the competitive concern immediately organized, the Tobacco Products Co., was capitalized at $40,000,000. A competitive steel concern, the Southwestern Steel Corporation, incorporated in May this year, was capitalized at $30,000,000. Recently, trade conditions stimulated production of crude petroleum, and a large number of new concerns were incorporated; but the capitalization almost uniformly exceeded $1,000,000. Independent oil interests in California, aiming to compete against Standard Oil in refining and marketing light oils, were compelled to organize themselves into an association, thereby limiting untrammelled competition. On June 23, the Pierce Oil Corporation incorporated with nominal capitalization, plans being for an ultimate capitalization of $40,000,000. Behind this concern are said to be the Rothschild interests who are credited with preparing to start a competitive war on Standard Oil. The Pierce incorporation was preceded early in June by an invasion of the California field by the Rothschild interests.

The steel industry is most typical of concentrated capital. The organization of the Steel Trust was not attended by the vicious and criminal practices of Standard Oil, nor did the Steel Trust attempt to crush its rivals and secure a monopoly. The Steel Trust and independents maintain friendly relations and co-operate. To-day the steel industry is undoubtedly the most efficient concentrated industry. The readjustive process aims to establish similar conditions in all industry: concentration, but not monopoly.

One of the objects of readjustment is to secure harmony between large producers and the end of cut-throat methods. Commenting on certain evidence in the government suit against the United Shoe Machinery Co., Financial America, a consistent apostle of concentration, said in its June 7, 1913, issue:

Here, if the conversations are true, we have a concrete illustration of the trust or monopoly in its most blighting and baneful aspect. First, we have an offer by the trust to buy out the offending competitor; second, a threat following the refusal of the trust’s terms; third, the “horrible example” of the perverse Parsons person, who rejected the trust’s terms; fourth, a delicate reminder that the “blue sky” will be the only covering left to the haughty independent when the trust gets through with him; and, fifth, the reference to the “wheel” upon which the trust breaks its victims. Could anything be more graphic, more persuasive, more deadly convincing of the fate in store for the independent marked out for slaughter? Nothing mealy-mouthed about such “stand and deliver” tactics; not a single wasted word. When one reads such testimony as this, his holiest desire should be a devout longing to see the men responsible for such intimidation contemplating a patch of “blue sky” from a barred cell window; while his every aspiration should be a prayer to strengthen the government’s arm in its attempt to strangle monopoly.

Roosevelt years ago sensed this spirit. In an Outlook article, more than two years ago, on “The Trusts, The People, And the Square Deal”, Roosevelt said:

“The letters from and to various officials of the Trust (Tobacco), which were put in evidence, show a literally astounding and horrifying indulgence by the Trust in wicked and depraved business methods such as the “endeavor to cause a strike in their (a rival business firm’s) factory,” or the “shutting off the market” of an independent tobacco firm by “taking the necessary steps to give them a warm reception,” or forcing importers into a price agreement by causing and continuing “a demoralization of the business for such length of time as may be deemed desirable” (I quote from the letters). A Trust guilty of such conduct should be absolutely disbanded, and the only way to prevent the repetition of such conduct is by strict governmental control, [Roosevelt has since demanded “administrative control”] and not merely by lawsuits.”

In an address at Newport, July 2 last, Roosevelt said that “in dealing with big corporations, as in dealing with all business. it is an absolute necessity for us to abandon the utter folly of discriminating against them on the ground of size instead of on the ground of conduct.” Roosevelt wishes to penalize the abuses of monopoly, and not concentrated industry itself.

Roosevelt advocates a regulation which would encourage concentration, but eliminate the unfair tactics pursued by plutocrats against lesser rivals. It is not accident that Roosevelt has repeatedly praised the Steel Trust; for this trust practices the Roosevelt idea–harmonious relations with its independent competitors. That is the relation Roosevelt would institute and enforce through “administrative control” of all business. Instead of business centralizing in a Morgan group, or any other private group, business is to centralize in the government through State Socialism and the control of an administrative despotism. Hand in hand with this goes government regulation and dictation of labor conditions, the chloroforming of proletarian action, and perhaps the legal prohibition of strikes.

The Roosevelt Progressive party program aims at the unity of capitalist interests, the strengthening of capitalist despotism, the crushing of the proletariat. And the economic facts favor that course.

With this political program, based on the new economic development, and the creation of a middle class of stock and bond owners in concentrated capital, all hope of assistance for the Revolution from the bulk of the middle class falls flat. While the conditions make political action on the part of the working class more imperative, seeing that economic issues will assume more and more of a political nature; even more imperative becomes the task of organizing the proletariat into the revolutionary army of integrated Industrial Unionism.

New Review was a New York-based, explicitly Marxist, sometimes weekly/sometimes monthly theoretical journal begun in 1913 and was an important vehicle for left discussion in the period before World War One. In the world of the Socialist Party, it included Max Eastman, Floyd Dell, Herman Simpson, Louis Boudin, William English Walling, Moses Oppenheimer, Walter Lippmann, William Bohn, Frank Bohn, John Spargo, Austin Lewis, WEB DuBois, Maurice Blumlein, Anton Pannekoek, Elsie Clews Parsons, and Isaac Hourwich as editors and contributors. Louis Fraina played an increasing role from 1914 on, leading the journal in a leftward direction as New Review addressed many of the leading international questions facing Marxists. The journal folded in June, 1916 for financial reasons. Its issues are a formidable archive of pre-war US Marxist and Socialist discussion.

PDF of full issue: https://www.marxists.org/history/usa/pubs/newreview/1913/v1n20-sep-1913.pdf